The world of electric two-wheelers can be a bit confusing. With new models emerging constantly, the lines between an "e-bike" and an "e-motorcycle" can seem blurry. However, understanding the distinctions is crucial, especially when it comes to something as important as insurance coverage.

Washington State recently enacted a new law that further clarifies the distinction between e-bikes and e-motorcycles. Effective June 11, 2026, electric bicycles in Washington must have fully operational pedals and cannot exceed 20 mph under motor power. Any electric cycle capable of traveling faster than 20 mph under motor power is now legally classified as a motorcycle and subject to motorcycle licensing, registration, and insurance requirements. We expect more states to follow and pass laws to regulate these new forms of transportation.

Let's break down the key differences and explore why those differences directly impact the type of insurance you'll need.

The Core Distinctions: Power, Speed, and Pedals

While both are electric and have two wheels, the primary differentiators between e-bikes and e-motorcycles lie in their power output, top speed capabilities, and the presence (and functionality) of pedals.

Electric Bicycles (E-Bikes)

E-bikes are designed to assist pedaling, not replace it entirely. They are essentially bicycles with an added electric motor.

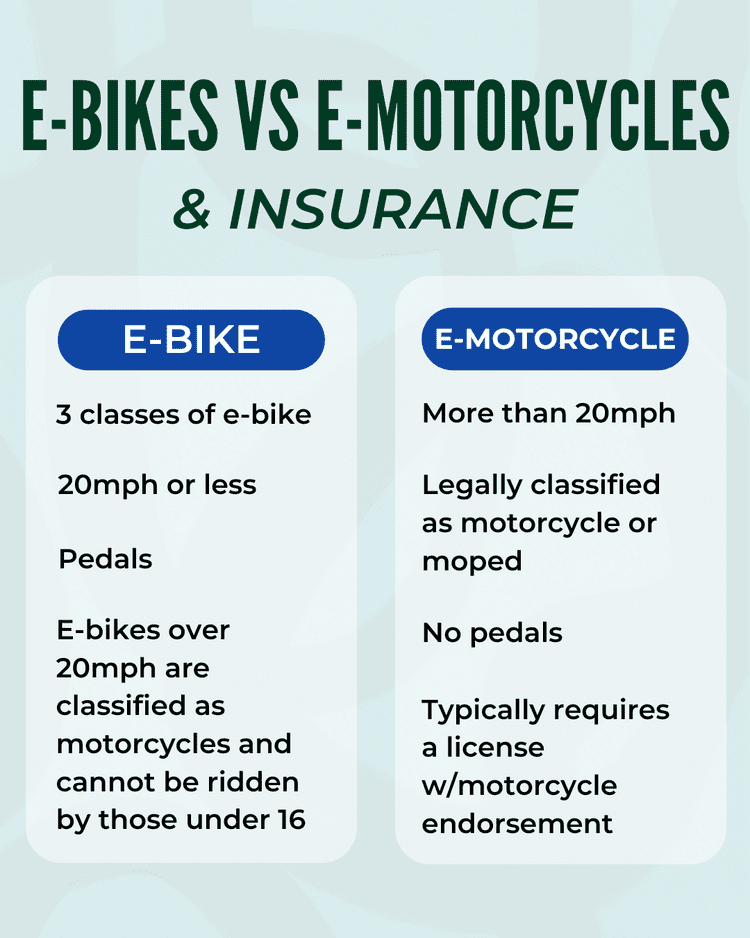

- Motor Power: E-bikes typically have motors with a maximum power output, often capped at 750 watts (regulations can vary by state).

- Speed: Under Washington's updated law, electric bicycles cannot exceed 20 mph under motor power. Once that speed is reached, the motor assistance must stop.

- Pedals: E-bikes must have fully functional pedals that are intended to be used. The motor provides assistance to your pedaling effort rather than serving as the sole means of propulsion.

- Classification: Washington's new law simplifies the distinction by requiring functional pedals and limiting motor-powered speed to 20 mph.

- Legality: E-bikes are generally allowed where bicycles are permitted, subject to local regulations. Riders should always check local trail, sidewalk, and pathway rules before operating an e-bike.

Electric Motorcycles (E-Motorcycles)

E-motorcycles, on the other hand, are built for speed and power, operating much like their gasoline-powered counterparts.

- Motor Power: They feature significantly more powerful motors, often measured in kilowatts (kW), capable of propelling the vehicle to much higher speeds.

- Speed: Electric motorcycles can easily exceed 20 mph under motor power and may reach highway speeds similar to traditional motorcycles.

- Pedals: Some models may resemble bicycles, but if the vehicle can exceed 20 mph under motor power, it is classified as a motorcycle regardless of appearance.

- Classification: Under Washington law, any electric cycle capable of exceeding 20 mph under motor power is legally classified as a motorcycle.

- Legality: E-motorcycles require a valid driver's license (and typically a motorcycle endorsement), vehicle registration, and motorcycle insurance. They are generally restricted to roads and highways rather than bicycle paths and trails.

Insuring an E-Bike or E-Motorcycle

When it comes to insurance, the primary difference between e-bikes and e-motorcycles is mandatory versus optional (although likely still very necessary).

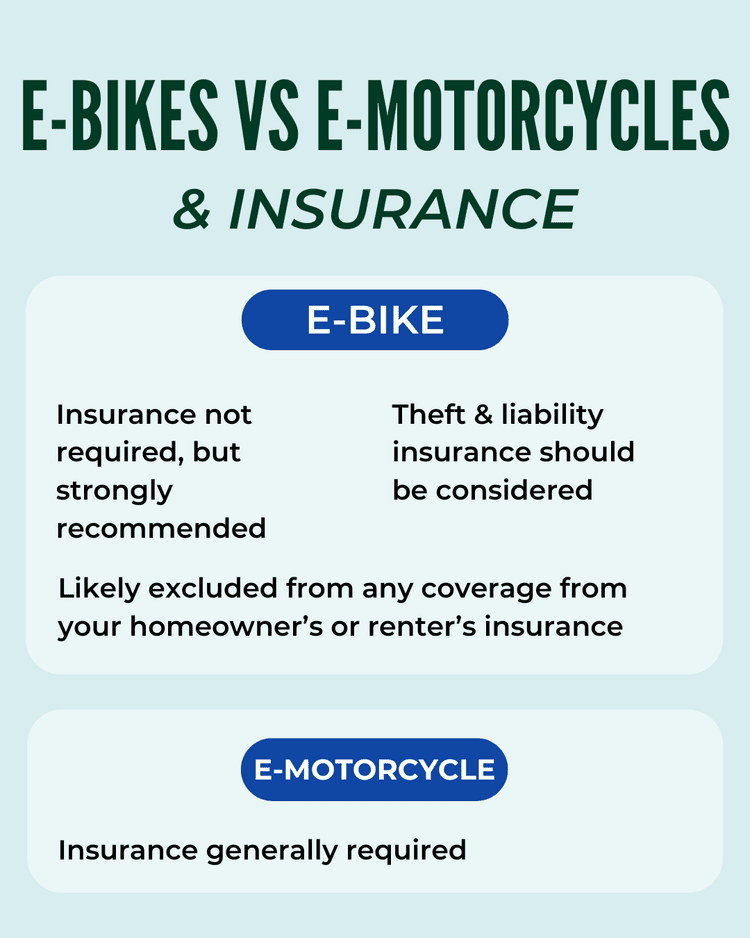

For standard, legal e-bikes that comply with Washington's requirements, insurance is generally not legally required, but it is highly recommended due to the high replacement cost and liability risk. Coverage for e-bike liability is not usually included with most renters or homeowners policies. Only bikes without power units or power assistance are typically included by renters and homeowner insurance policies.

For e-motorcycles, the rules are clear: they are treated like their gasoline-powered counterparts, which means insurance is generally required to legally operate the vehicle on public roads. All motorcycles are excluded from coverage by renters and homeowners insurance policies.

Theft of an E-Bike

Standard homeowners and renters policies often exclude or have significant limitations when it comes to e-bike coverage. In fact, don't assume your homeowners or renters policy fully covers your e-bike.

E-bikes are expensive, often costing several thousand dollars, making them attractive targets for thieves. Without proper insurance, replacing your e-bike could be a significant financial burden.

If you have an endorsed or expanded homeowners and renters policies you might need to know the following limitations:

- Limited coverage for theft if the bike has anytime of power assistance.

- Depreciated value of the bike not replacement cost (~60% of value).

- Limited liability coverage subject to maximum speed, value of bike and rider type (child vs adult or household member vs permissive rider).

If your e-bike is stolen while commuting, traveling, or parked away from your residence, coverage may be limited or unavailable depending on your policy.

Injury to Others & Property Damage

Even compliant e-bikes can travel at speeds capable of causing serious injuries or property damage.

If you accidentally injure someone or damage property while operating your e-bike, you could be held legally liable for medical expenses, repairs, legal costs, and other damages.

Liability coverage can help protect you financially if an accident occurs.

Separate E-Bike or E-Motorcycles Policies Recommended

Whether you have an e-bike or an e-motorcycle we recommend that you consider a stand-alone motorcycle policy covering the physical damage and the liability for these risks. Here are some of the reasons why:

- Motorcycle policies cover liability, physical damage and medical coverage for the owner and any guest riders.

- Physical damage deductibles are lower with motorcycle policies compared to a homeowners policy.

- There is no claim penalty that puts your home insurance in jeopardy.

- You can cover multiple e-bikes, e-motorcycles and e-scooters on the same policy.

- Riding gear like helmets and other protection gear are usually included on a motorcycle policy.

Tips for Protecting Your E-Bike

- Invest in high-quality locks and use them every time you leave your bike unattended.

- Register your e-bike if a local registration program is available.

- Add identifying markings and consider installing a GPS tracker.

- Follow safe riding practices and obey local traffic laws.

- Take a bicycle safety course to stay current on changing regulations.

- Some courses may even qualify you for insurance discounts.

- Before purchasing an e-bike, verify that it complies with Washington's updated legal requirements.

- If you let someone borrow your e-bike make sure you understand if a “permissive rider” has liability or physical damage coverage under your insurance policy.

Consult Your Trusted Insurance Advisor

As electric bicycle technology continues to evolve, so do the laws governing their use. Washington's new e-bike law creates a clearer distinction between e-bikes and e-motorcycles, making it more important than ever to understand how your vehicle is classified and what insurance coverage may be appropriate.

We recommend consulting your trusted insurance advisor before purchasing an e-bike or e-motorcycle to ensure you have a comprehensive understanding of your coverage options.

Call or text us with any questions about e-bike or e-motorcycle insurance, we're here to help!