Davidson & Associates Insurance Blog

All You Ever Wanted to Know About Insurance

Is Your Vehicle Ready for Winter Weather?

Monday, December 1, 2025

Winter is coming with cold temperatures, fog, snow and ice. Now is the time to prepare your vehicle for hazardous conditions and treacherous driving. Try these 6 tips to be ready: 1. Ensure fluids are at the proper...

Melissa Ralston Earns Safeco Insurance Award of Excellence for Superior Underwriting Skills

Wednesday, November 26, 2025

Davidson & Associates Insurance’s Vice President of Personal Lines, Melissa Ralston, has earned this year's Safeco Insurance Award of Excellence. As the most prestigious underwriting recognition Safeco® independent...

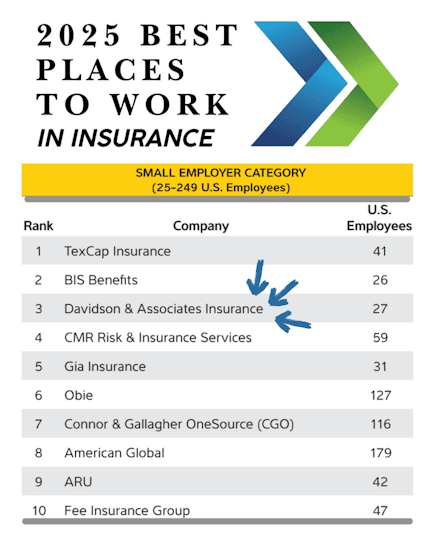

Davidson & Associates Insurance Named in Business Insurance’s Annual Best Places to Work in Insurance

Monday, November 10, 2025

Davidson & Associates Insurance has been named “Best Places to Work in Insurance,” ranking #3 in the nation for the category of small business. This award recognizes employers for their outstanding performance in...

Is Your Home Ready for "The Big One"? A Sober Look at Earthquake Insurance

Monday, October 27, 2025

Living in the Pacific Northwest is a trade-off. We get the stunning mountains, the evergreen forests, and the dramatic coastline. In exchange, we live with the quiet, looming knowledge that we are in serious earthquake...

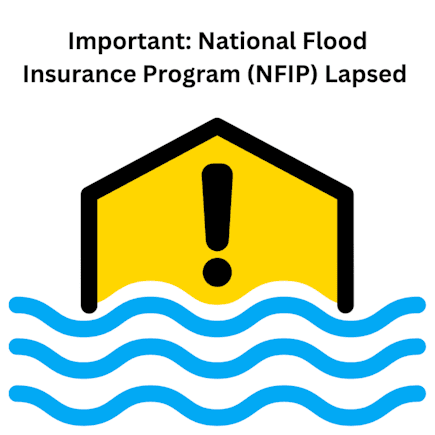

NFIP Has Lapsed Due to Government Shutdown

Wednesday, October 1, 2025

As of midnight on September 30, 2025, the National Flood Insurance Program (NFIP) has NOT been reauthorized by Congress, resulting in an official program lapse due to the ongoing government shutdown. This lapse has...

QBE's Departure from the Home Insurance Market

Friday, September 26, 2025

The insurance landscape is constantly shifting, and when a major player like QBE decides to exit a significant market segment, it sends ripples throughout the industry. Recently, QBE announced its decision to cease...

Best Insurance Agency in Clark County

Monday, September 15, 2025

Davidson & Associates Insurance is proud to announce they have been named Best Insurance Agency by the Columbian’s 2025 Best of Clark County. This is the second year in a row earning the title of Best Insurance...

Davidson & Associates Insurance Named a 2025 Best Practices Agency

Friday, August 22, 2025

Davidson & Associates Insurance Agency has earned the 2025 Best Practices Agency status, joining an elite group of independent insurance agencies from across the United States. The Best Practices Agency designation...

What Is Ensuing Loss Coverage for Your Boat, Yacht, or Marina?

Wednesday, July 30, 2025

Hanging out at the yacht club, you may have heard your sailing buddies talking about ensuing loss coverage for their vessels. If you’re not familiar with this clause in many marine insurance policies, this post is for...

Pet Insurance: Coverage for Sickness, Accidents & Wellbeing

Tuesday, July 22, 2025

Insurance for Your Pet in Sickness and in Health If you’re a pet owner, you‘ve probably heard a lot about health insurance for pets and may have already purchased it. If you want to insure your pet’s health, it’s...

What Is Hull Agreed Value and How Does It Affect Your Marine Policy?

Wednesday, July 16, 2025

When you purchase boat or yacht insurance, one of the main components - alongside liability protection - is coverage for replacing the boat itself if something happens to it. Many marine policies use agreed value for...

Sign & Glide Coverage or Emergency Assistance: How Does It Work?

Wednesday, June 25, 2025

If you purchase boat or yacht insurance, you may be asked about adding emergency assistance protection, sometimes known as “Sign & Glide” coverage. Here’s what you need to know about this type of marine insurance,...

Contractors, Do You Have Marine Liability?

Wednesday, June 11, 2025

If you’re a contractor who works on certain types of marine construction or waterside projects, you need extra insurance protection for unique scenarios. If you don’t have marine liability coverage, you could find your...

Yacht Coverage: Be Sure Your Investment Is Fully Protected

Wednesday, May 28, 2025

If you own a yacht, having the right insurance is essential. Without it, you could face significant out-of-pocket expenses. Or worse, you could be responsible for serious liability costs. In this article, we review what...

How to Effectively Insure Your Marina

Wednesday, May 14, 2025

Every marina is unique. But one thing they all have in common is the need for the right insurance in case the unexpected happens. You’ll have greater peace of mind knowing your business is protected from the special...

Homeowner’s Insurance Does Not Cover Cryptocurrency Theft

Tuesday, April 8, 2025

Most homeowner’s policies have a small sublimit for currency and coins stored in a home, typically around $500. However, that coverage does not extend to cryptocurrency or cyber tokens for physical goods. There are a...

Davidson & Associates Named “Best Company to Work For”

Tuesday, January 21, 2025

For the third year in a row, Davidson & Associates Insurance proudly takes home the title of “Best Companies to Work For” in the category of small businesses presented by the Seattle Business Magazine. Reflecting...

Davidson & Associates Insurance is an independent insurance agency located in Vancouver, Washington.

Give us a call, make an appointment, or request a quote online to find out how much we can save you on your insurance.

Contact Us

- 11112 NE 51st Circle

Vancouver, WA 98682 - 360-514-9550

- 360-514-9551

- Mon-Thu 9am-5pm

Friday 9:00am - 4:00pm

© 2026 Davidson & Associates Insurance | Search | Privacy | Disclaimer | Accessibility | Website by BT